The Cut Through Quarterly Q1 2026 Australian Startup Funding Report provides a detailed view of Australian startup funding activity in the first quarter of 2026. The report examines capital raised, venture and accelerator round activity, sector performance, valuation trends, investor sentiment, startup maturity, portfolio health, and funding outcomes for female founders.

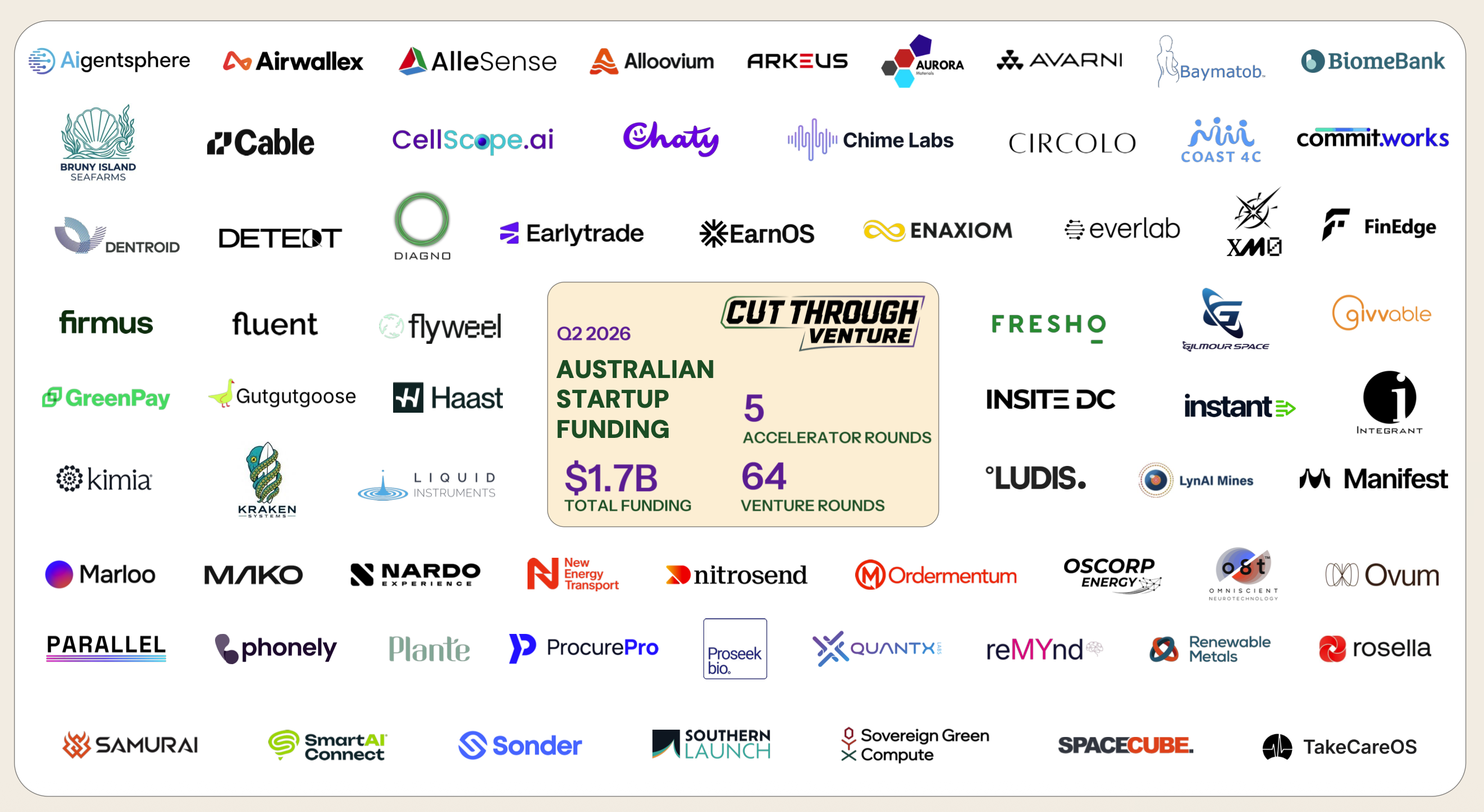

Q1 2026 opened with Australia’s strongest first-quarter funding result since the 2022 peak, with $1.8 billion in announced funding across 81 venture rounds and 26 accelerator rounds. However, the report shows that the recovery remains highly selective, with a small number of large deals accounting for a substantial share of total capital.

Key headline numbers

$1.8B in total announced startup funding\

81 venture rounds

26 accelerator rounds

Strongest Q1 funding result since 2022 market peak

Funding was 63% on Q1 2025

Funding was more than double levels recorded in Q1 2024 and Q1 2023

Market interpretation

The report notes that the market is “open for business again,” but remains selective. Capital is being deployed, yet investors are concentrating larger cheques into companies with stronger conviction, defensibility, traction, or capital-intensive ambitions.

Five Things to Know from Q1 2026

1. Funding rebounded, but selectively

Australia’s startup ecosystem recorded a strong start to the year, with $1.8B raised across 107 total rounds, including both venture and accelerator activity. The recovery was not broad-based across all companies, with investors remaining selective.

2. Mega-rounds drove the headline number

The top end of the market had an outsized impact on the quarter.

The top 10 deals accounted for almost 60% of all capital raised

The top 20 deals represented 79% of total capital

The largest single deal accounted for 11% of Q1 funding

Sub-$10M rounds contributed their lowest share of capital in five years across Q4 2025 and Q1 2026

3. Capital is moving beyond traditional SaaS

While software remains central to the Australian startup ecosystem, many of the quarter’s largest rounds were in categories such as:

- Space and defence

- Hardware, robotics and sensors

- Cybersecurity, compliance and digital identity

- AI models and data infrastructure

- Life sciences and biotech

- Climate and energy

This reflects a broader shift toward companies embedded in physical-world systems and critical infrastructure.

4. AI is now embedded across the ecosystem

The report introduces a revised sector taxonomy to reflect AI’s growing presence across categories rather than treating it only as a standalone sector.

AI-first and AI-enabled companies accounted for more than half of Q1 deals

Startups with an AI component attracted the majority of both capital and deal activity

AI-first companies were especially common at Accelerator and Pre-Seed stages

Investors reported valuation premiums for companies where AI materially improves the product, economics, or customer workflow

5. Startups are raising earlier, but graduating later

The report finds that companies are raising their first funding rounds at younger ages, while later-stage rounds are taking longer to reach.

Median age at Pre-Seed dropped to 1.1 years

Median age at Seed was 2.5 years

Median age at Series A rose to 6.7 years

Median age at Series B increased to 9.7 years

The journey from Pre-Seed to Series B has nearly tripled in length since 2021

Deal Activity and Capital Concentration

Q1 2026 was one of the most concentrated quarters in recent years. While the headline funding result was strong, the broader deal environment remained uneven.

Largest funding categories by capital raised

Vertical business software: $447M

Hardware, robotics and sensors: $303M

Space and defence: $229M

Cybersecurity, compliance and digital identity: $125M

Crypto, Web3 and stablecoins: $113M

AI models and data infrastructure: $100M

Consumer brands: $80M

Climate and energy: $79M

Horizontal business software: $78M

Healthtech: $76M

Mega-rounds reshaped the market picture

The largest deals of the quarter included substantial rounds across space, defence, hardware, AI infrastructure, cybersecurity, and vertical software. The report highlights this as a sign that Australian venture funding is increasingly flowing into companies with physical infrastructure, national capability, or deep technical defensibility.

A New Cohort of Australian Unicorns

Q1 2026 saw the emergence of a new cohort of Australian unicorns that differ from the previous generation of SaaS and fintech leaders.

New unicorns highlighted in the report

Advanced Navigation — AI-enabled navigation and autonomous systems for defence and industrial applications; A$1.5B valuation

Gilmour Space — sovereign launch capability through vertically integrated rocket manufacturing and launch services; A$1.5B valuation

Neara — infrastructure modelling software for utilities and grid resilience; A$1.1B valuation

The report notes that these companies are deeply embedded in physical-world systems, marking a departure from earlier Australian unicorns that were largely defined by SaaS and fintech.

Deal Sizes and Valuation Trends

Q1 2026 showed a clear increase in cheque sizes from Seed through Series A, while smaller rounds continued to shrink.

Median deal sizes by stage

Angel + Pre-Seed: $1.2M

Seed: $6.1M

Series A: $12.5M

Series B+: $27M

Round-size trends

Sub-$5M rounds fell to their lowest quarterly level since 2020

$5M–$19.9M rounds increased to 27

$20M–$49.9M rounds increased to 13

$50M+ rounds rose to 10

The report characterises the market as more selective rather than inactive. Larger rounds are still getting done, but they are being concentrated behind companies that clear a higher investor bar.

AI-First Startups Command a Valuation Premium

Investor sentiment indicates that AI-first companies are receiving higher valuations than non-AI peers, even as broader valuation expectations remain measured.

Investor views on AI valuation premiums

45% of investors said AI-first startups were valued somewhat higher than non-AI peers

40% said AI-first startups were valued significantly higher

Only 13% said there was no difference

No investors reported AI-first startups receiving lower valuations

Seed valuations and SAFE caps

Cake Equity data included in the report shows early-stage pricing strengthened into Q1 2026.

Median seed valuation reached $16M

Median SAFE cap reached $15M

Median seed valuation increased 35% versus the 2025 average

Median seed valuations more than doubled from $7.7M in Q1 2024 to $16.0M in Q1 2026

Sector Trends in Q1 2026

Vertical software still leads, despite the shift toward “atoms”

Vertical business software remained the largest category by both capital raised and deal count.

$447M raised across vertical business software

30 deals in the category

More than half of vertical software deals were Seed or earlier

Vertical software attracted strong investor interest due to workflow depth, domain context, and industry-specific distribution

Hardware, robotics and sensors gained significant momentum

Hardware, robotics and sensors represented the second-largest category by capital raised.

- $303M raised

- 17 deals

- Strong representation across large rounds

- Investors identified hardware, deep tech, and quantum as areas of growing global opportunity

Horizontal SaaS faces more pressure

The report identifies a widening gap between vertical and horizontal software.

Vertical software captured 80% of software capital

Vertical software represented 76% of software deals

Horizontal software captured 20% of software capital

Horizontal software represented 24% of software deals

50% of investors rated vertical software as exciting

Only 2% of investors rated horizontal software as exciting

The report links this divide to AI’s effect on defensibility, with horizontal SaaS more exposed to replication and commoditisation.

Investor Sentiment and Portfolio Health

Investor optimism softened compared with prior periods, even though funds remain active and continue to prioritise new investments.

Investor sentiment

43% of investors expected to do more deals than last year

42% expected about the same number of deals

15% expected fewer deals

55% rated deal flow quality as good

2% rated deal flow quality as excellent

Investor priorities

The top priorities for the quarter were:

Investing in new startups

Ensuring current portfolios remain well capitalised

Fundraising from LPs

Marketing and business development

Internal initiatives

Portfolio health

The report shows portfolios have stabilised, but pressure remains.

70% of investors rated portfolio health as good

10% rated portfolio health as excellent

20% rated portfolio health as fair

82% reported no portfolio company shutdowns in the past quarter

13% reported one shutdown

5% reported two or more shutdowns

Startup Maturity and the Longer Path to Series B

The report’s maturity analysis shows that Australian startups are beginning their venture journeys earlier but taking longer to progress to later-stage funding.

Median company age at funding stage

Pre-Seed: 1.1 years

Seed: 2.5 years

Series A: 6.7 years

Series B: 9.7 years

What this suggests

The report suggests later-stage companies may be spending early capital more carefully, extending runway, and returning to market with more mature proof points. This may reflect both investor expectations and founder preferences in a more disciplined funding environment.

Female Founder Funding Outcomes

Female founder and mixed-gender teams raised $205M in Q1 2026. This was down from Q4 2025 but broadly in line with longer-term averages.

Female founder activity by sector

Female founder and mixed-gender teams were most active in:

Vertical business software: 7 deals

Hardware, robotics and sensors: 4 deals

Life sciences and biotech: 4 deals

Fintech: 3 deals

Climate and energy: 2 deals

Largest female founder funding categories

Consumer brands: $67M from 1 deal

Hardware, robotics and sensors: $51.8M from 4 deals

Life sciences and biotech: $47.1M from 4 deals

Vertical business software: $17.5M from 7 deals

Fintech: $15.2M from 3 deals

Stage-level participation

Female founder and mixed-gender teams reached an all-time high at Pre-Seed in both deal share and capital share, but participation weakened at later stages.

Female-only teams were absent from Series A and later rounds

Mixed-gender teams carried all recorded female founder participation at Series A and later

Growth-stage participation remained volatile